If buyer’s remorse isn’t afflicting Trump backers, it should be

Ray Bradbury was onto something in “Fahrenheit 451.” He gave us a protagonist, Guy Montag, who was a fireman – but hardly in the conventional sense. Montag’s job was to set fire to homes that housed books. The reason: ignorance was essential to dominating society.

That seems to be something Donald J. Trump understands quite well.

When Trump was elected, some readers were irked at a column in this space that suggested that economic ignorance among his supporters helped drive his victory. The piece argued that Trump’s backers didn’t understand the causes and remedies for inflation, didn’t grasp the dangers of tariff threats, and didn’t understand how chaos in the Oval Office could put our country under a cloud.

Trump was happy to exploit that ignorance, as he promised to quash rising prices, enrich the country through tariffs and kill the “deep state” that he contended was holding America down.

Well, might some of those Trumpers be having just a bit of buyer’s remorse now?

After all, the stock market under Trump has reflected anything but optimism. As of the market close on March 11, the much-watched S&P 500 index had dropped nearly 6.4 percent since Trump was inaugurated. The tech-heavy NASDAQ composite index had plunged even more, some 11 percent, and the Dow had lost 3.6 percent. On March 12, NASDAQ index eked out a 1.2 percent gain for the day and the S&P 500 index bounced up nearly a half point, but the Dow slipped another 0.2 percent.

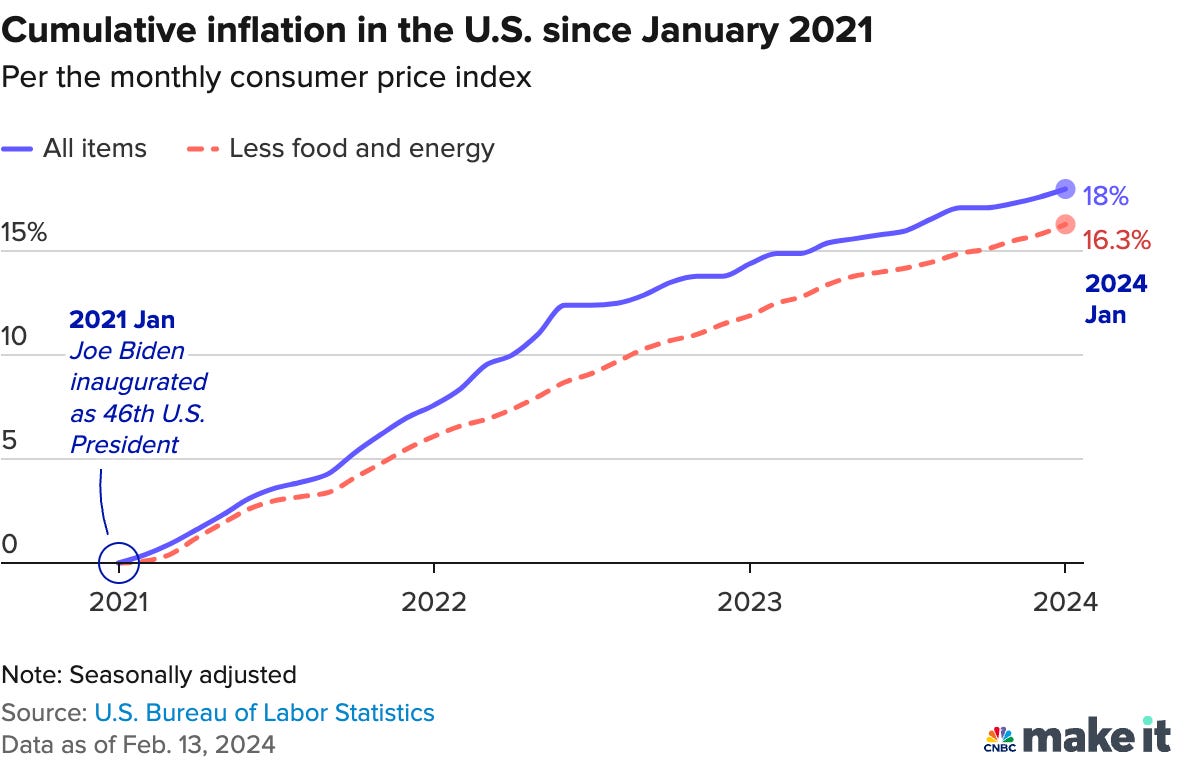

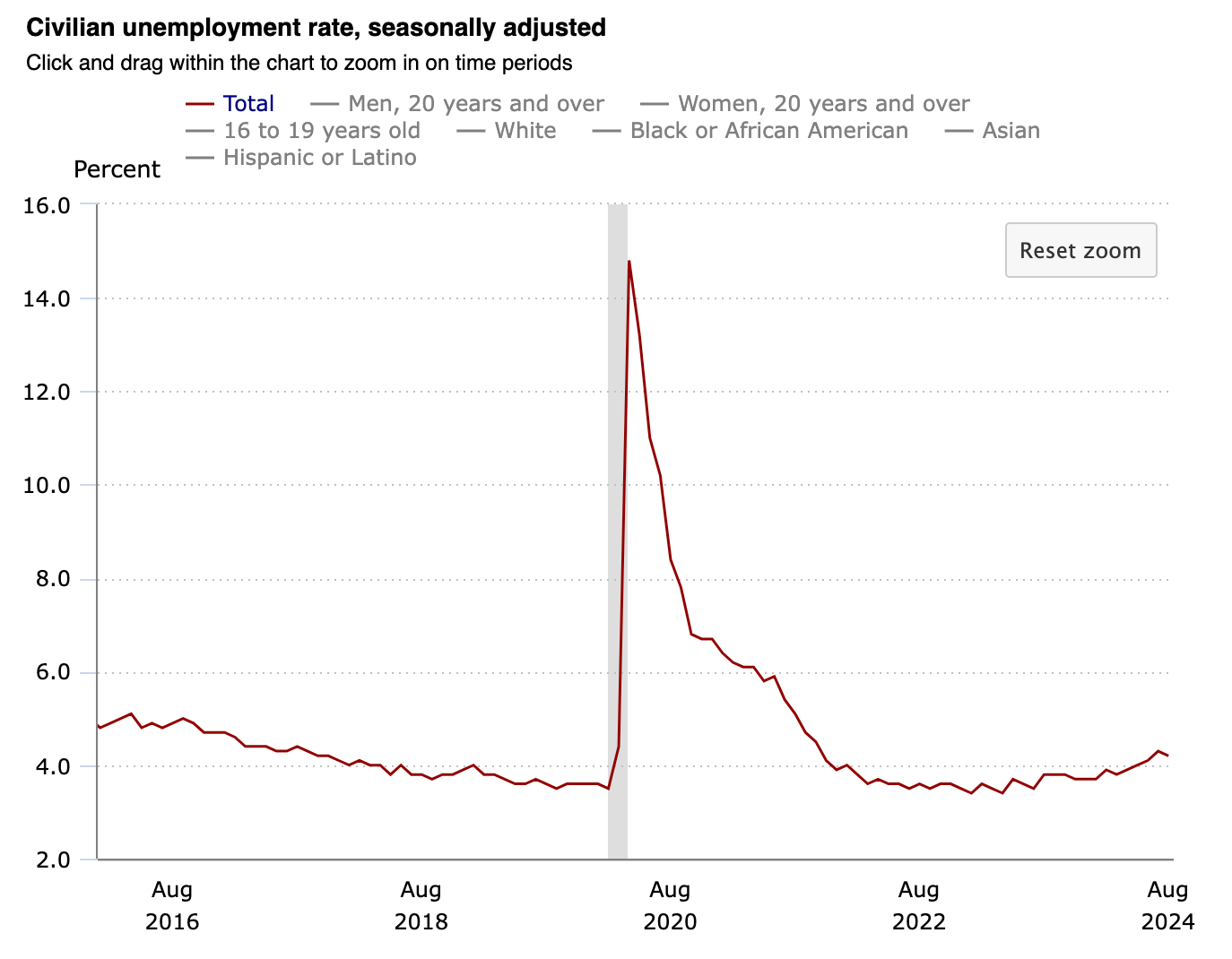

What’s more, inflation has hardly been tamed. Beyond the avian-flu-related price of eggs, the inflation rate turned upward a half-percentage point in January and another 0.2 percent in February. Also, there’s precious little to crow about in job-creation, with a weaker-than-expected jobs report in February that helped nudge the unemployment rate up to 4.1 percent, as labor force participation slipped.

And dour outlooks seem to be spreading. Consumer sentiment has tumbled to a 15-month low, as layoff announcements shot up to a 4.5-year high, as Forbes reported.

That all means the Federal Reserve, fearful of contributing to more inflation, is standing pat on interest rates, with its repeated rate cuts of last year now very much in the rearview window. In the dry language of the folks at J.P. Morgan, “The Fed is likely to hold off on further decreases in interest rates in the near-term as it assesses the strength of the U.S. economy within the backdrop of heightened fiscal policy uncertainty.”

Uncertainty, indeed. So much so that people are using the “R word.” Talk of recession is in the air.

“The economy will likely suffer a downturn if the Trump administration follows through on the tariff increases it has announced and maintains those tariffs for more than a few months,” Mark Zandi, chief economist of Moody’s Analytics, posted on X. And Jonathan Millar, senior economist at Barclay’s told USA Today that if Trump imposes all his planned tariffs, “then we’ll probably get a recession.”

Even Trump refuses to rule out the possibility that his policies – especially his on-again off-again threats of tariffs against allies and adversaries alike – could plunge the United States into a downturn. In fact, he seems to be softening up Americans for a rough road by saying the country is in a “period of transition” and his earlier comment that Americans could feel “some pain” from his burgeoning trade wars.

It’s no wonder that investors – who, after all, put down markers on the future with every stock buy or sell – are heading for the exits. And it’s no wonder that forecasters are getting more jittery than they’ve been in months.

Zandi told ABC News that his firm raised its gauge of the probability of a recession to 35 percent. “That’s uncomfortably high — and it’s rising,” Zandi said.

And Goldman Sachs boosted the odds of a recession in the coming 12 months up from 15 percent to 20 percent. More pessimistically, J.P. Morgan Chase economists pegged the chances of a recession this year at 40 percent – up from 30 percent at the opening of the year — citing “extreme U.S. policies,” Bloomberg reported.

To be sure, many such forecasters have proven to be Chicken Littles in the past. In the halcyon days of Biden’s term, during the summer of 2023, Goldman’s crystal ball signaled a more than 30 percent chance of a recession, according to Forbes. That was just before the U.S. “ripped off seven consecutive quarters of more than 1.5% GDP growth and the stock market surged, even as monetary policy remained restrictive.”

Moreover, economists such as Paul Krugman are arguing that talk of a “Trumpcession” is premature. The data so far don’t suggest that, he holds, even while he warns of “a palpable sense of disappointment in the Trump economy.”

Nonetheless, a slowdown – if not a full-blown recession – seems very much on the horizon. Even before the latest Trump-induced tumult, the Congressional Budget Office, for instance, was expecting a meager 1.9 percent gain in GDP this year and 1.8 percent the following year, down from 2.3 percent last year. And The Conference Board sees decelerating growth throughout the year, ending with the economy eking out a 1.7 percent gain in the closing quarter.

The problem is not so much ignorance among Trumpers – who, perhaps, can be forgiven for that, given the state of economic education in our schools. Instead, the problem is ignorance in the Trump Administration that is driving its growth-threatening policies.

As the president stubbornly clings to his tariff policies – imposing a 25 percent levy on Canadian steel and aluminum, even while backing down from a threat to double that figure – do he and his advisers not really appreciate the market disruption they are causing? Are they blind to the declines Trump is spawning in the retirement kitties of millions of Americans?

Certainly, he doesn’t seem to care much.

“Markets are going to go up and they’re going to go down. But you know what? We have to rebuild our country,” Trump told reporters, according to USA Today. He made the comment as he promoted Tesla vehicles alongside Elon Musk, the CEO of Tesla and the guy driving widespread government layoffs.

Can both men be so dense? As soon as legislators oblige him, Trump plans to kill a $7,500 federal tax incentive for electric cars. So, it’s no surprise that investors are giving the stink eye to Tesla, one of the leading makers of such cars, paring its share price from above $424 a share on Inauguration Day to below $231 recently.

And is it helping to “rebuild our country” to lay off tens of thousands of federal workers, with at least 62,530 of them dismissed in the opening two months of this year alone, by one recent count? And that doesn’t include the just-announced nearly 50 percent cut in the staff of the Department of Education, bringing that unit down to fewer than 2,200 people. That department provides money, such as Pell Grants, to students to attend college and funds elementary and secondary schools nationwide.

Is it helping when Trump imposes tariffs that are triggering retaliation from around the world against American farmers and other producers? The trade war he has launched promises to be costly for everyone, companies and consumers alike.

Canada, the largest steel supplier to the U.S., will slap 25 percent reciprocal tariffs on American steel products and raise taxes on tools, computers and servers, display monitors, sports equipment, and cast-iron products, for instance. The European Union, similarly responding to Trump’s measures, will raise tariffs on American beef, poultry, bourbon and motorcycles, peanut butter and jeans.

Prices will rise across the world. “We deeply regret this measure,” said European Commission President Ursula von der Leyen. “Tariffs are taxes. They are bad for business, and even worse for consumers.”

So much for the battle against inflation.

The U.S. last endured a brief recession during Trump’s first term, with the downturn lasting from February to April 2020. The economy at that point was slammed by the dawn of the Covid epidemic.

Now it seems the economy is taking body blows from tariffs, federal workforce reductions and a decline in consumer attitudes. If a “Trumpcession” isn’t imminent, is it unavoidable over time under such pressures? Unless Trump and his minions get a crash course in economic sanity, they might find out the hard way. That may give his supporters plenty of reason for doubt.